May 2026

A busy week in HealthTech: four moves across pharma, outpatient, hospital and consumer, each reshaping who owns the clinical workflow

Founder & CEO, HGM Advisory

Key takeaway

Three structural shifts are playing out simultaneously. First, consumer health wearables (Whoop, Oura, Fitbit) are being overtaken by companies using blood work and imaging for prediction (Function Health, Neko Health), with an eventual convergence likely. Second, SAP's exit from the hospital market forces 250 German hospitals to choose between legacy systems, AI-native platforms like Avelios, or modular open stacks (Vitagroup, Better) — a defining moment for German hospital IT. Third, Roche's acquisition of PathAI must be evaluated against the underperformance of Foundation Medicine and Flatiron Health, with stakeholders questioning whether Roche can avoid repeating the pattern in digital oncology.

A weekly roundup of three major HealthTech developments: the wearables category is pivoting from fitness tracking toward clinical-grade prediction, Doctolib and AI-native platforms are reshaping the provider tech stack as SAP exits the hospital market, and Roche's acquisition of PathAI raises questions about its digital oncology track record after Foundation Medicine and Flatiron.

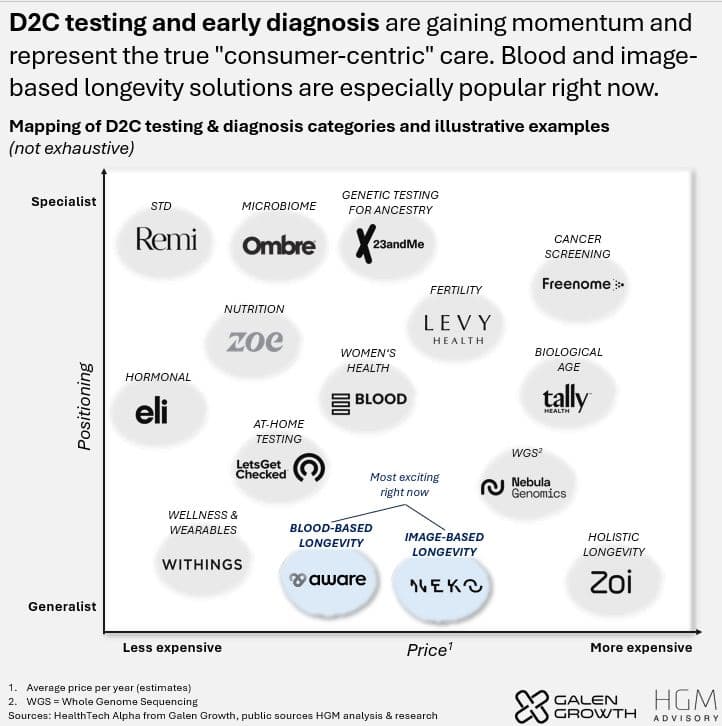

Why are wearables pivoting from fitness to clinical prediction?

The promise that "wearables will revolutionize healthcare" has not materialized despite years of investment. Companies like Whoop, Oura, and Fitbit continue to innovate on hardware and algorithms, but the category remains largely confined to fitness and wellness rather than clinical decision-making. The data these devices collect — heart rate, sleep patterns, activity levels — has not yet translated into the kind of predictive clinical insights that would make wearables indispensable in healthcare delivery.

The real shift is happening adjacent to traditional wearables. Companies like Function Health and Neko Health are using blood work and full-body imaging to build predictive health profiles that go far beyond what a wrist-worn sensor can capture. Function Health offers comprehensive blood panels with AI-driven analysis, while Neko Health uses body scanning technology for early disease detection. The convergence thesis is that these approaches will eventually merge: wearable continuous monitoring combined with periodic deep diagnostics (blood, imaging) could create a genuinely predictive health platform. But as of May 2026, these remain separate categories with different business models and clinical evidence bases.

How is Doctolib reshaping the European provider tech stack?

Doctolib has fundamentally reshaped France's Practice Management System (PMS) market, capturing over 20% market share against legacy leaders that had dominated for decades. The company achieved this by starting with patient booking — a high-frequency, low-friction entry point — and expanding backward into the full practice management workflow. This is the classic wedge strategy: own the patient relationship first, then absorb the administrative and clinical layers.

In Germany, Doctolib has now launched its own PMS product, entering a market that is simultaneously being disrupted from another direction. AI-native platforms are gaining traction, building practice management from scratch with AI at the core rather than adding AI features to legacy architectures. The combination of Doctolib's proven playbook and the emergence of AI-native competitors is creating unprecedented competitive pressure on incumbent German PMS vendors at exactly the moment when practices are most open to switching.

What does SAP's hospital market exit mean for German healthcare IT?

SAP's decision to exit the hospital market forces approximately 250 German hospitals to make a critical technology choice in the near term. These hospitals must decide between three paths: migrating to another traditional hospital information system vendor, adopting an AI-native platform like Avelios that reimagines hospital IT from the ground up, or building a modular open stack using interoperability-focused companies like Vitagroup and Better.

This is a defining moment for German hospital IT. The hospitals affected by SAP's exit cannot simply delay the decision — they need a functioning system. This creates a rare window where a significant number of hospitals are simultaneously evaluating their entire technology stack, rather than the usual incremental upgrade cycle. For AI-native hospital IT companies, this is the largest addressable market opportunity in German healthcare in years. The choices these 250 hospitals make over the next 12-18 months will shape the competitive landscape of German hospital IT for a decade.

Can Roche deliver on digital oncology after Foundation Medicine and Flatiron?

Roche's acquisition of PathAI must be evaluated in the context of the company's track record with previous digital health acquisitions. Foundation Medicine (acquired 2018) and Flatiron Health (acquired 2018) were both positioned as transformative bets on data-driven oncology. Foundation Medicine would use genomic profiling to match patients with targeted therapies, while Flatiron would use real-world evidence from electronic health records to accelerate drug development and improve treatment decisions.

Neither acquisition has delivered on its original promise at the scale initially projected. Foundation Medicine remains a strong diagnostics business but has not transformed oncology treatment selection at the systemic level. Flatiron's real-world evidence platform has been valuable for regulatory submissions but has not fundamentally changed how oncology drugs are developed or prescribed. The question with PathAI is whether Roche has learned from these experiences or whether the same pattern will repeat: acquire a promising digital health company, integrate it into a pharma organizational structure that prioritizes drug development timelines over platform innovation, and watch the original vision narrow. Stakeholders across digital oncology may also resist Roche's growing dominance in this space, preferring open platforms to a single company controlling diagnostics, real-world evidence, and now pathology AI.

About the author

Thomas HagemeijerFounder & CEO of HGM Advisory. Management consultant and HealthTech expert working across the full healthcare ecosystem: pharma, MedTech, investors, startups, hospitals, and policymakers. Investor at Springboard Health Angels. Ambassador at HLTH Europe and HBI. Regular keynote speaker on AI in healthcare and digital health transformation.

Related insights

January 2025

Neko Health raises $260M at $1.8B: the rise of D2C clinical healthcare

March 2026

Tech x Outpatient Care: Heidi, Doctolib and Eterno are redefining the ambulatory tech stack

April 2026

HealthTech x Providers: the scale-ups redefining hospital and ambulatory care in Germany

September 2025

Healthcare Tech Stack: AI redefines hospitals & outpatient care