March 2025

European HealthTech ecosystems: France leads funding, but capital alone does not build champions

Founder & CEO, HGM Advisory

Key takeaway

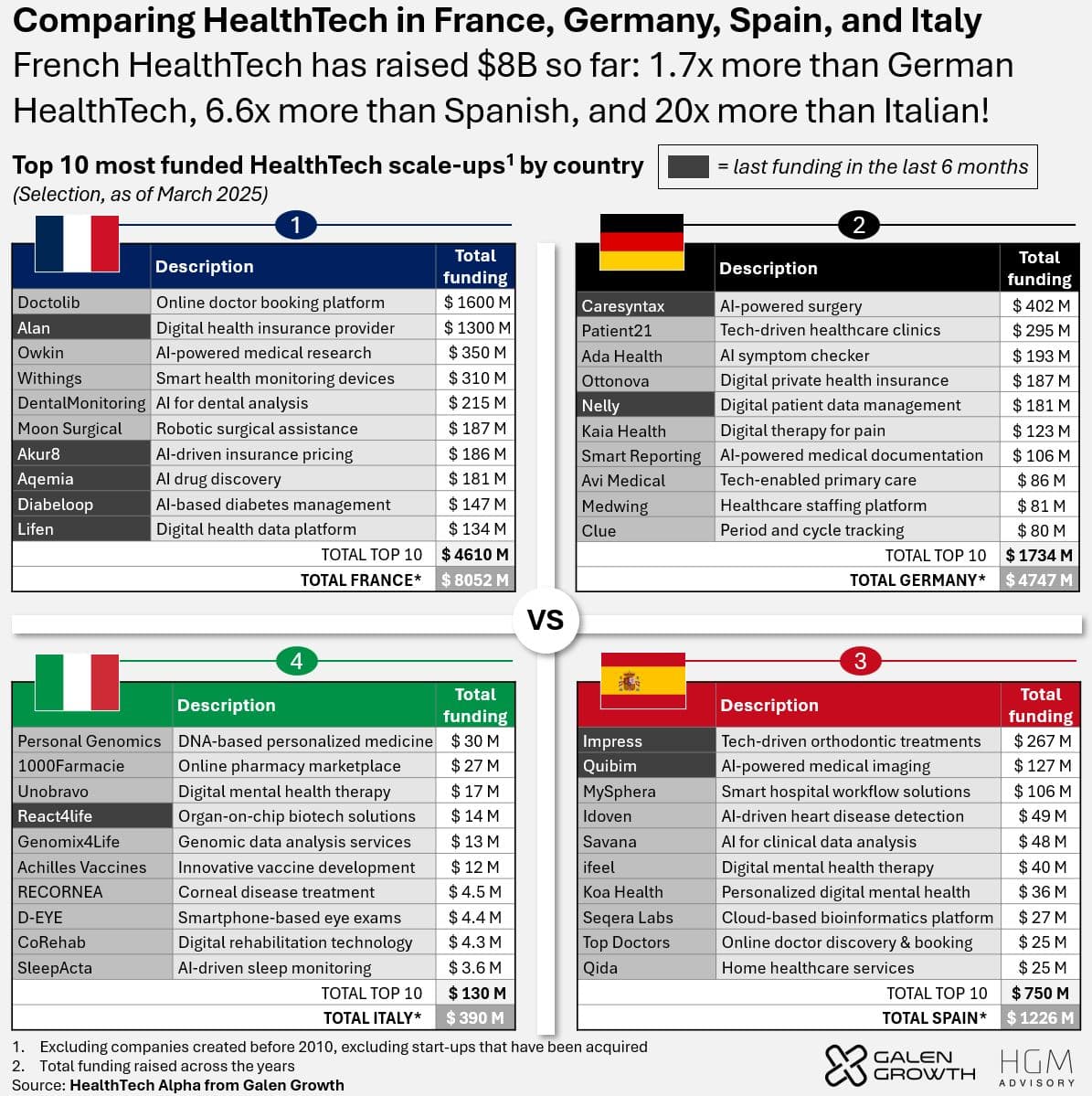

France leads European HealthTech funding with Doctolib (~$870M) and Alan (~$800M, 700K members, EUR 500M+ ARR), but building European champions requires more than capital. Strong networks, supportive policies, and the upcoming EHDS regulation will determine which ecosystems produce the next generation of scaled companies.

A comparative analysis of HealthTech ecosystems across France, Germany, Spain, and Italy. France leads funding (Doctolib ~$870M, Alan ~$800M), but ecosystem maturity depends equally on networks, policies, and industry trust. The EHDS will accelerate cross-border expansion.

The funding landscape across Europe

European HealthTech funding remains concentrated in a handful of countries. Excluding the UK, the ranking is: France, Germany, Switzerland, Sweden, Spain, Netherlands, with Italy at 12th. This does not correlate with healthcare market size, where Germany leads, followed by France, Italy, and Spain.

France's dominance is driven by two outliers: Doctolib (~$870M raised, dominant in patient scheduling across France, Germany, and Italy) and Alan (~$800M raised, 700,000 members, EUR 500M+ ARR). Without these two companies, France's position looks significantly less dominant.

Spain offers an interesting counterpoint: with roughly 8x less funding than France, Spanish HealthTech companies must be dramatically more capital-efficient. Portugal's Sword Health ($3B valuation) demonstrates that Southern European companies can reach global scale with the right model.

Why funding alone does not build ecosystems

Three factors beyond capital determine ecosystem strength.

First, networks: the density of connections between founders, clinicians, investors, and corporate buyers accelerates deal flow and knowledge transfer. France benefits from a tight Parisian HealthTech community; Germany's ecosystem is more fragmented across Berlin, Munich, and Hamburg.

Second, policies: regulatory frameworks that enable innovation (like France's early adoption of telehealth reimbursement) create market pull that capital alone cannot. Germany's complex KV system and conservative digital health adoption have slowed ecosystem development despite larger healthcare spending.

Third, industry trust: healthcare is a relationship business. Ecosystems where founders have credibility with hospital administrators, payers, and regulators move faster than those where HealthTech is still viewed with skepticism.

The EHDS effect and cross-border expansion

The European Health Data Space regulation will be the most significant catalyst for European HealthTech ecosystem development. By standardizing health data exchange across EU member states, EHDS removes one of the biggest barriers to cross-border scaling: data fragmentation.

For HealthTech companies, EHDS means a product validated in France can be deployed in Germany without rebuilding the data integration layer from scratch. For investors, it means the addressable market for any European HealthTech company effectively becomes the entire EU rather than a single country.

We expect accelerated M&A activity as companies seek to build pan-European positions before EHDS implementation deadlines. The companies that establish cross-border footprints now will have a decisive advantage.

About the author

Thomas HagemeijerFounder & CEO of HGM Advisory. Management consultant and HealthTech expert working across the full healthcare ecosystem: pharma, MedTech, investors, startups, hospitals, and policymakers. Investor at Springboard Health Angels. Ambassador at HLTH Europe and HBI. Regular keynote speaker on AI in healthcare and digital health transformation.